If you have ever stared at an Explanation of Benefits and wondered why the number the insurance company paid looks nothing like the number the hospital charged, you have just brushed against the single most important concept in the entire revenue cycle. That concept is the allowed amount in medical billing.

By definition, the allowed amount in medical billing is the maximum dollar figure that a health insurance plan agrees to pay for a specific covered healthcare service. It is the contractually negotiated ceiling, and it is the only number that actually governs what gets reimbursed, regardless of what a provider originally charges.

It goes by several names depending on who is talking about it. Your insurer might call it the "negotiated rate," the "contracted rate," or the "eligible expense." Medicare calls its version the "Medicare Approved Amount." Whatever the label, the function is identical: it defines the outer boundary of reimbursement for any given service.

Here is what makes the allowed amount so consequential: once a provider joins an insurance network and signs a participation agreement, they are legally bound to accept the allowed amount as payment in full for covered services. The provider cannot bill the patient for the difference between what was charged and what the payer approved. That difference gets written off entirely. Understanding this single fact reframes how you read every single claim that flows through your practice.

Why Does This Number Exist?

Insurance companies and government payers exist within a fee schedule framework. Without a standardized, contractually set rate, every provider could charge any amount for any service, making claims impossible to process consistently at scale.

The allowed amount creates predictability for payers, controls costs for employers and patients, and gives providers a known reimbursement baseline when they join a network. It is the economic spine of the entire U.S. healthcare payment system.

Practices that understand the allowed amount deeply are the ones that catch underpayments faster, reduce claim denials, and protect revenue that would otherwise leak silently out of the revenue cycle. HMS Medical Billing Services works inside this number every single day, and this guide is the distilled version of what we know.

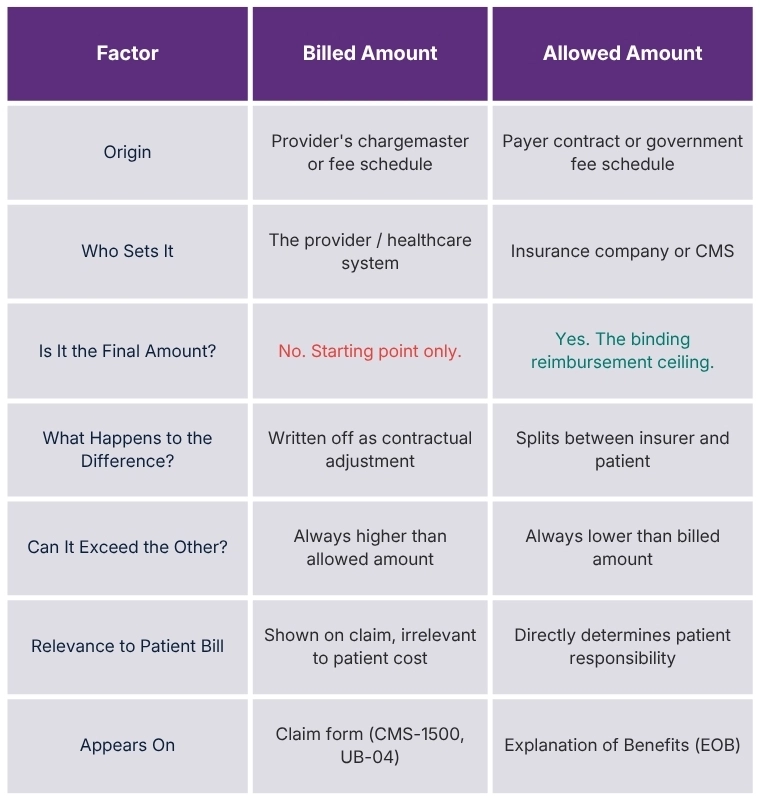

Billed Amount vs. Allowed Amount Why They Are Never the Same

The gap between the billed amount and the allowed amount is one of the most misunderstood realities in healthcare finance. Patients see it on their EOBs and assume something went wrong. New billers see it and wonder if the claim was underpaid. Neither reaction is usually correct, but the confusion costs everyone time and money.

The Billed Amount

The billed amount is whatever the provider submits on the claim. It originates from the provider's chargemaster, the internal price list that assigns a dollar figure to every service, procedure, supply, or room charge in the facility.

Chargemaster rates are typically set significantly above what any payer is expected to actually pay. They serve as an opening position in the financial negotiation that the contracting process represents.

This is why hospital billed charges can seem absurd to patients. A facility might list a routine blood draw at $400 because the chargemaster was built to accommodate the lowest expected negotiated rate from any of their payers while still generating enough margin to sustain operations. The chargemaster is a starting point, not a price anyone is expected to pay in full.

The Allowed Amount

The allowed amount is the negotiated rate. It is what was agreed upon before the patient ever walked through the door, codified in the contract between the provider and the payer. When the claim comes in, the payer applies the allowed amount to the covered service and ignores the billed charge entirely.

The difference between the billed amount and the allowed amount becomes the contractual adjustment, also called the write-off. In-network providers are contractually required to write this amount off and cannot pass it to the patient.

The Allowed Charge Definition

The terms "allowed amount" and "allowed charge" are used interchangeably across the industry, but they carry a slightly different connotation worth understanding.

The allowed charge definition, at its most precise, refers to the pre-determined fee that a payer will apply to a specific service code when adjudicating a claim.

The distinction matters in practice because some payers use "allowed charge" specifically when describing services that are covered and eligible for reimbursement, separating them from services that are non-covered.

If a service is non-covered, there is no allowed charge because the payer simply refuses to recognize the claim at all. If a service is covered, the allowed charge is the negotiated fee that governs how the payment is calculated.

Example:

Think of the allowed charge definition this way: it is the payer saying, "For CPT code 99213, our contract says the maximum reimbursable fee is $94.16. Everything above that gets written off. Of that $94.16, you will receive 80% from us and collect the remaining 20% from the patient as coinsurance." Every dollar flowing out of that claim traces back to this single negotiated figure.

Allowed Amount vs. Maximum Out of Pocket

Patients frequently confuse the allowed amount with their out-of-pocket maximum. These are entirely different concepts.

The allowed amount is the maximum the payer will recognize for a service. The out-of-pocket maximum is the ceiling on what the patient will pay across all covered services in a plan year.

After the patient hits their out-of-pocket maximum, the insurer covers 100% of the allowed amount for remaining covered services. The allowed amount itself does not change; what changes is who pays it.

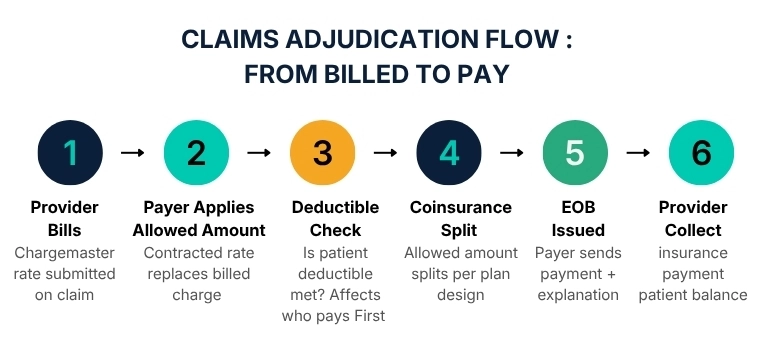

What is the Allowed Amount Calculation Formula in Medical Billing

Once the allowed amount is established for a given claim, it does not go entirely to the provider or entirely to the insurer. It gets split according to the patient's benefit plan design. The three elements that govern that split are the deductible, the coinsurance, and the copay.

Allowed Amount = Insurance Payment + Patient Responsibility

Insurance Payment = Allowed Amount × Coinsurance %

Patient Responsibility = Allowed Amount × Patient Coinsurance %

(Plus any unapplied deductible balance)

Write-Off = Billed Amount − Allowed Amount

The Role of the Deductible

Before coinsurance kicks in, the patient must first satisfy their annual deductible. If a patient has a $1,500 deductible and has paid $0 so far in the plan year, the first $1,500 of allowed charges goes entirely to the patient, and the insurer pays nothing on those claims until the deductible is met. Once it is met, the coinsurance formula takes over.

The Role of Copays

Some plans use a flat copay structure instead of percentage-based coinsurance for certain service types, particularly office visits and prescriptions. When a copay applies, the patient pays the flat amount defined in their plan, and the insurer pays the remainder of the allowed amount. The copay is collected at the time of service. It counts toward the out-of-pocket maximum, but it does not reduce the allowed amount itself.

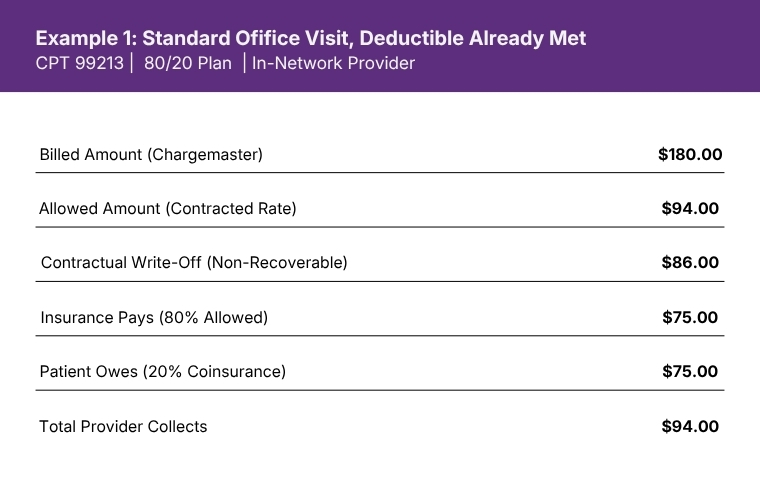

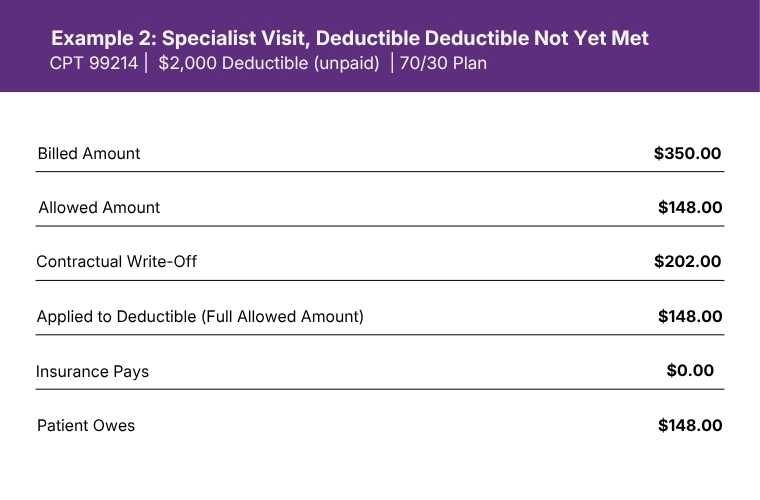

Allowed Amount Examples

Theory without numbers is just vocabulary. Here are four distinct scenarios that show exactly how allowed amounts translate into actual cash flow for providers and patients across different plan designs.

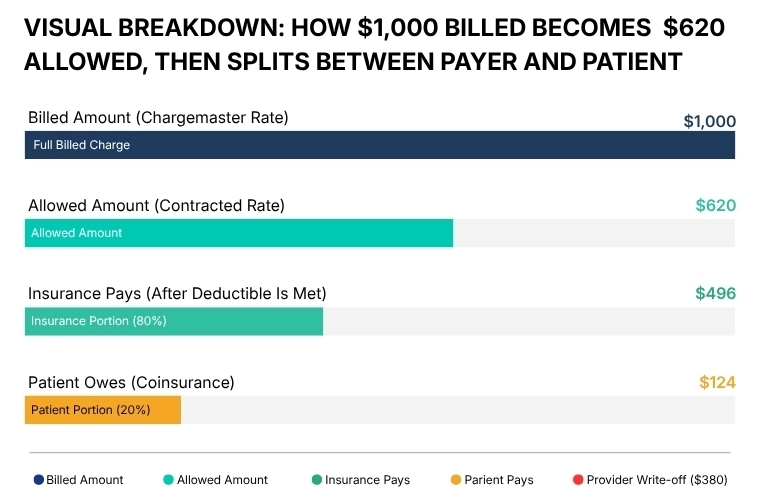

The provider billed $180 but is contractually bound to accept $94 as payment in full. The $86 write-off is the price of being in network. The insurer and patient together cover the full $94 allowed amount.

When the deductible is not yet met, the patient pays the entire allowed amount. The insurer pays nothing on this claim. The write-off still applies. The provider collects $148, not $350.

How Payers Actually Set the Allowed Amount

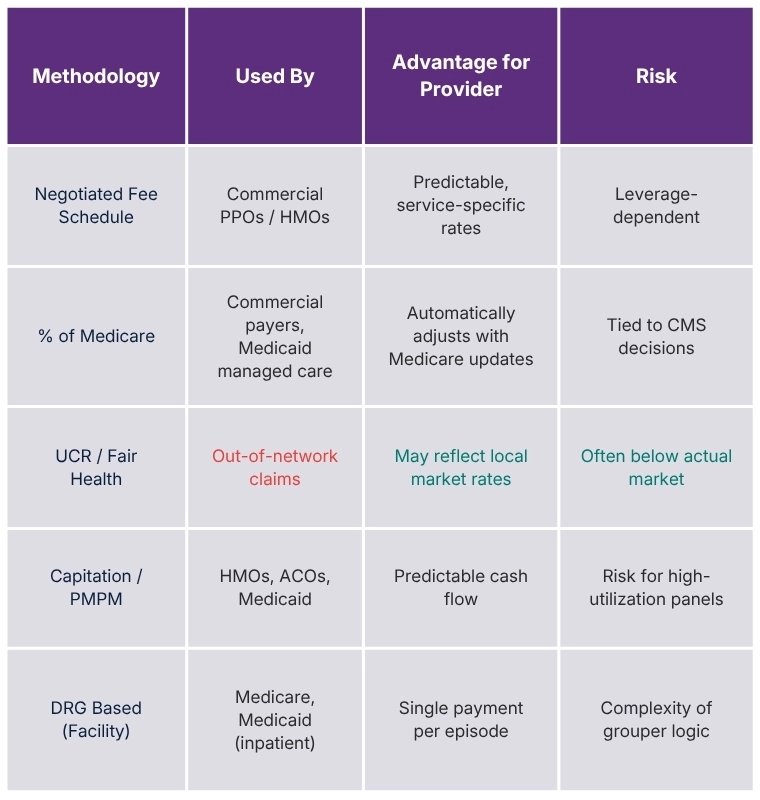

The allowed amount does not appear out of thin air. Payers use several distinct methodologies to arrive at these rates, and knowing which methodology your payer uses is one of the most powerful pieces of intelligence a billing team can hold.

Fee Schedule Negotiation

For commercial insurers, the most common mechanism is direct contract negotiation. The insurer and the provider or provider group sit across from each other and negotiate a fee schedule, service by service or as a percentage of another reference rate. Larger provider groups with significant market share negotiate higher rates. Solo practices and small groups often have limited leverage and accept near-standard rates.

Percentage of Medicare

Many commercial payers establish their allowed amounts as a percentage of the Medicare fee schedule. A commercial insurer might agree to pay 120% of the Medicare allowed amount for a given service. This creates an elegant efficiency: as Medicare updates its fee schedule annually, the commercial contract rates automatically adjust without requiring full renegotiation. Providers should always know what percentage of Medicare their major commercial contracts represent.

Usual, Customary, and Reasonable (UCR) Rates

Some payers, particularly for out-of-network claims, rely on UCR databases to establish what they consider an appropriate payment level. These databases aggregate claim data across geographic regions and service types to define what a "reasonable" charge looks like for a given service in a given market. Fair Health and HIQS (formerly Ingenix) are two of the most commonly referenced UCR databases. UCR-based rates are frequently lower than what in-network contracts produce, which is part of what makes out-of-network claims financially painful for patients.

Value-Based and Capitation Models

In value-based contracts and capitated payment models, the concept of the allowed amount per service becomes less relevant because payment is structured around per-member-per-month fees or global episode bundles rather than individual service reimbursements. However, even in these arrangements, fee-for-service benchmarks anchored to allowed amounts are frequently used for reconciliation and quality bonus calculations.

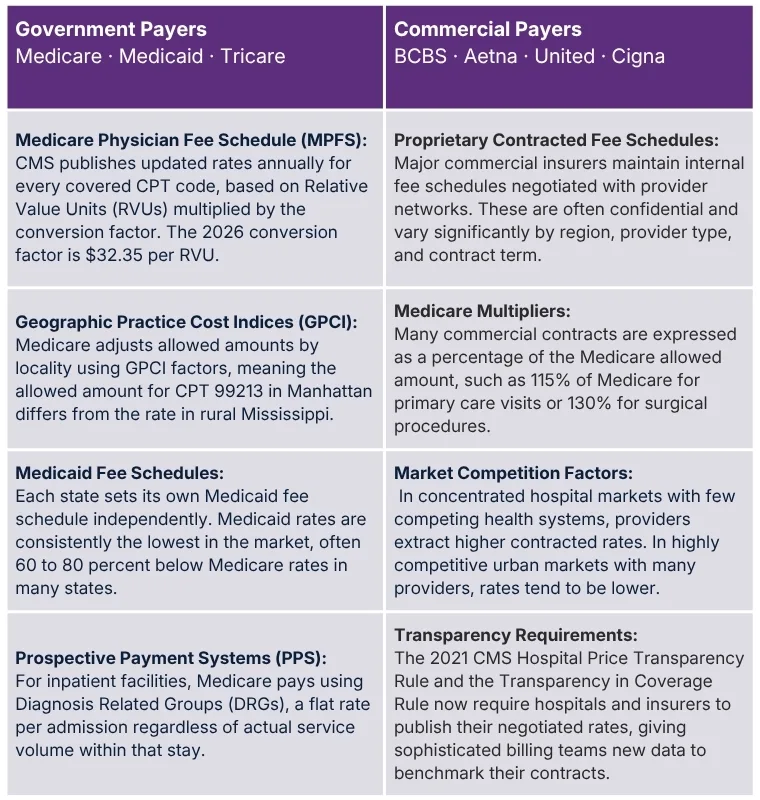

Primary Sources for Setting Allowed Amounts for Commercial

Medicare Physician Fee Schedule (MPFS): CMS publishes updated rates annually for every covered CPT code, based on Relative Value Units (RVUs) multiplied by the conversion factor. The 2026 conversion factor is $32.35 per RVU.

Geographic Practice Cost Indices (GPCI): Medicare adjusts allowed amounts by locality using GPCI factors, meaning the allowed amount for CPT 99213 in Manhattan differs from the rate in rural Mississippi.

Medicaid Fee Schedules: Each state sets its own Medicaid fee schedule independently. Medicaid rates are consistently the lowest in the market, often 60 to 80 percent below Medicare rates in many states.

Prospective Payment Systems (PPS): For inpatient facilities, Medicare pays using Diagnosis Related Groups (DRGs), a flat rate per admission regardless of actual service volume within that stay.

Proprietary Contracted Fee Schedules: Major commercial insurers maintain internal fee schedules negotiated with provider networks. These are often confidential and vary significantly by region, provider type, and contract term.

Medicare Multipliers: Many commercial contracts are expressed as a percentage of the Medicare allowed amount, such as 115% of Medicare for primary care visits or 130% for surgical procedures.

Market Competition Factors: In concentrated hospital markets with few competing health systems, providers extract higher contracted rates. In highly competitive urban markets with many providers, rates tend to be lower.

Transparency Requirements: The 2021 CMS Hospital Price Transparency Rule and the Transparency in Coverage Rule now require hospitals and insurers to publish their negotiated rates, giving sophisticated billing teams new data to benchmark their contracts.

The No Surprises Act and Its Impact on Allowed Amount Disputes

Effective January 1, 2022, the federal No Surprises Act fundamentally changed the out-of-network billing landscape. For emergency services and certain non-emergency services at in-network facilities, providers can no longer balance bill patients beyond their in-network cost-sharing amounts, even when the provider is out of network. Instead, a federal Independent Dispute Resolution (IDR) process governs how payers and providers settle the final payment amount.

The IDR process uses the Qualifying Payment Amount (QPA), typically defined as the payer's median contracted rate for the service in the same geographic region, as a key reference point. Arbitrators in the IDR process must start from the QPA and consider additional factors to arrive at a final allowed amount for the disputed claim.

Practices engaged in significant out-of-network billing, particularly in specialties like emergency medicine, anesthesiology, and radiology, should have expert audit and compliance support in place to navigate these regulatory requirements.

Why Some Providers Stay Out of Network Intentionally

Certain specialists, particularly in high-demand procedural specialties, deliberately remain out of network with specific payers to avoid low contracted rates. These providers often negotiate directly with patients using prompt-pay discounts or require upfront payment and assist patients in filing for out-of-network reimbursement from their insurers. This model works for providers with sufficient patient volume and market reputation, but it carries significant revenue cycle complexity and patient access risk.

What Really Happens When You Charge More Than the Allowed Amount

This is the section that most billing guides skim over. The consequences of exceeding contractual allowed amounts range from inconvenient to catastrophic, depending on whether the behavior is isolated or systematic. Here is the full picture.

1- Mandatory Write-Off

For in-network providers, any billed amount above the contracted allowed amount is automatically adjusted off as a contractual adjustment. The payer will not pay it. The provider cannot bill the patient for it. It is gone. This is expected and normal within the billing cycle, not a violation.

2- Balance Billing ViolationsAttempting to collect the write-off amount from the patient, knowingly or not, constitutes illegal balance billing. State laws and the No Surprises Act create significant patient and regulatory protections. Violations can result in state licensing complaints, payer contract termination, and civil liability.

3- Payer AuditsSystematic patterns of billing above the expected charge level relative to local benchmarks can trigger payer audits. Payers have sophisticated analytics that flag providers whose billing patterns deviate from peer norms. An audit can result in recoupment demands, prepayment reviews, and in severe cases, contract termination.

4- Medicare and Medicaid SanctionsFor government payers, systematically billing above the Medicare or Medicaid allowed amount with intent to defraud triggers the False Claims Act. Penalties under the False Claims Act include up to three times the damages plus civil monetary penalties per false claim. These violations are investigated by the OIG and DOJ.

5- Contract TerminationRepeated violations of contract terms, including attempts to collect above the allowed amount, give payers grounds to terminate the provider agreement. Losing a major commercial contract can immediately impact revenue by 10 to 30 percent or more depending on the payer mix.

6- Recoupment DemandsWhen payers discover overpayments, they issue recoupment demands that allow them to offset future claims payments. A single audit cycle can result in millions of dollars in retroactive

recoupment across multiple years of claims. This cash-flow disruption can be devastating for smaller practices.

⚠️ Critical Compliance WarningBilling above the allowed amount is not always intentional. Chargemaster errors, outdated fee schedules, coding mistakes, and insufficient staff training are the most common root causes. The legal system does not always distinguish intent from outcome when evaluating False Claims Act liability. Proactive billing audits are the most effective defense. HMS Audit Services helps practices identify and correct these vulnerabilities before they escalate.

When the Allowed Amount Works Against You: Underpayments and How to Fight Them

The discussion so far has focused on the provider charging more than the allowed amount. But the reverse situation, where the payer pays less than the contractually required allowed amount, is at least as common and often far more damaging to practice revenue because it is far less visible.

Underpayments occur when a payer applies an incorrect allowed amount to a claim. This can happen because the payer's fee schedule data is outdated, because the claim was miscategorized during adjudication, because modifier logic was applied incorrectly, or simply because of systematic payer errors that are never corrected unless the provider disputes them.Industry research consistently shows that between 3 and 11 percent of all claims are underpaid at any given time, depending on payer mix and claim complexity. For a practice billing $2 million annually, that can represent $60,000 to $220,000 in annual revenue walking out the door silently.

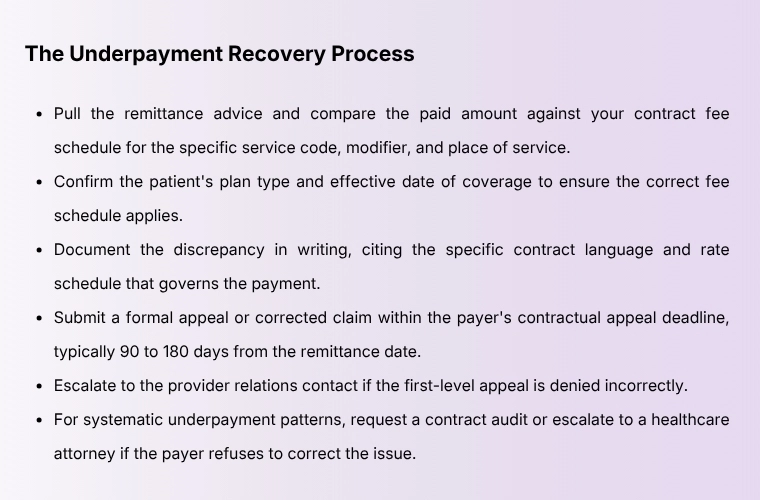

How to Detect Underpayments

The only reliable way to catch underpayments is to compare the payer's remittance against the contracted allowed amount for each service code. This requires having current, verified copies of every payer contract and fee schedule loaded into your billing system for automated comparison. When the payment posted does not match the contracted rate, a dispute should be initiated promptly, as timely filing limits apply to appeals just as they do to original claims.

Our medical billing services team performs contractual variance analysis as a standard component of payment posting, flagging every remittance that deviates from contracted rates. Across our client portfolio, this process recovers a meaningful percentage of revenue that would otherwise be silently accepted as accurate payment.

What Every Provider Should Know and Do Right Now

Understanding the allowed amount in medical billing is not just academic. It directly shapes how much revenue a practice retains, how patients experience their financial responsibility, and whether the billing team catches money that belongs to the practice.

Know Your Allowed Amounts Before You See the Patient

The most powerful moment to understand the allowed amount is before the claim is submitted. Insurance verification should include not just eligibility and benefits but also a lookup of the payer's estimated allowed amount for the planned services. This gives front-desk staff accurate information to communicate to patients about their expected financial responsibility before care is delivered. Surprises on the patient side generate delays in payment and damage the patient relationship.

Our Virtual Front Desk team performs real-time insurance verification that includes benefit-level detail, giving practices the information they need to set accurate patient expectations at every appointment.Credentialing Affects Your Allowed Amount Access

A provider who is not credentialed with a payer is effectively out of network with that payer, even if they work within an in-network group practice. Claims submitted under a non-credentialed provider NPI will either be denied outright or processed at out-of-network rates. The resulting lost revenue and patient exposure can be dramatic. Proper medical credentialing services ensure that every provider in your practice has current, accurate, active enrollment with every relevant payer before a single claim is filed.

Audit Your Contracts Annually

Payer contracts are not permanent. Allowed amounts can change when contracts are renegotiated, when Medicare fee schedules are updated, or when Medicaid state plans are revised. A fee schedule that was accurate 18 months ago may be producing systematic underpayments today. Annual contract audits, cross-referenced against actual remittances, are essential for practices that want to protect their full contractual revenue.

Coding Accuracy Is Revenue Protection

Every CPT code maps to a specific allowed amount. A code billed at the wrong level of evaluation and management produces an allowed amount that does not reflect the work actually performed. Downcoding costs practices real money on every single claim it affects. Our medical coding team applies AMA guidelines and payer-specific coding rules to ensure every service is captured at the highest defensible level of specificity and complexity.

Understand Your Payer Mix and Its Impact on Average Allowed Amounts

Every practice has a payer mix, the percentage of volume coming from Medicare, Medicaid, commercial PPOs, HMOs, and self-pay patients. Because each payer type has dramatically different allowed amounts for the same service, your payer mix directly determines your average reimbursement per unit of work. A practice with 40% Medicaid volume will have a significantly lower blended allowed amount than a comparable practice with 40% commercial volume.

Strategic payer mix management, understanding which contracts to prioritize, which to renegotiate, and which to exit, is a core function of a sophisticated revenue cycle strategy. Practices serving multiple states should also pay attention to geographic variation in allowed amounts across their locations.

Whether you operate a solo or private practice, a hospital system, or a home health agency, the principles governing the allowed amount are identical. What changes is the scale of the consequences when they are misunderstood.Words By Author

The allowed amount in medical billing is not a footnote in the revenue cycle. It is the revenue cycle. Every claim your practice files, every payment your billing team posts, and every dollar your patients owe traces directly back to this one figure. When you understand it at this level, you stop reacting to billing problems and start preventing them.

That is precisely where HMS USA LLC was built to operate. From verifying benefits before the first appointment to catching the underpayment that slipped through on a Tuesday afternoon remittance, we work inside the allowed amount every hour of every day so your practice does not have to guess.

ABOUT AUTHOR

Carlos Andrew

As a blog writer with years of experience in the healthcare industry, I have got what it takes to write well-researched content that adds value for the audience. I am a curious individual by nature, driven by passion and I translate that into my writings. I aspire to be among the leading content writers in the world.