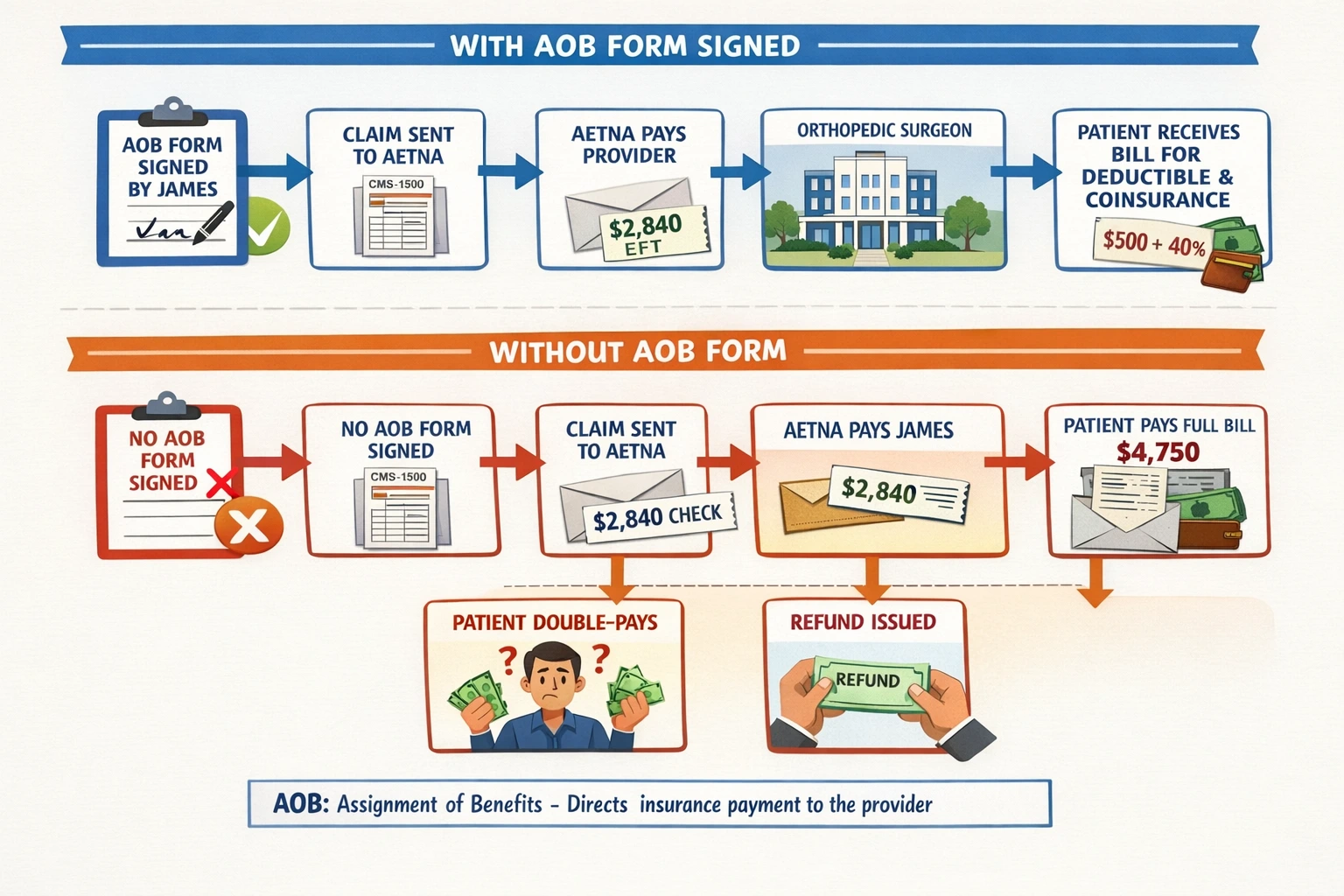

Here is a scenario that plays out in hundreds of practices every week: a patient gets treated, the insurer processes the claim, and a reimbursement check lands in the patient's mailbox instead of the provider's bank account.

The patient cashes it. The practice spends the next 60 days chasing the money, sending statements, fielding calls, maybe involving collections. Revenue delayed. Staff hours burned.

This entire situation is preventable. The fix is a single document executed properly at intake: the Assignment of Benefits form.

But AOB in medical billing is not as simple as getting a signature on a form. There are anti-assignment clauses buried in payer contracts.

There is CMS-1500 box placement that determines whether insurers even route payment to you. There are state-specific regulations that can render your AOB unenforceable overnight. And there is the ABN/AOB confusion that causes compliance headaches in Medicare billing.

This guide covers all of it written for people who already understand the basics and need the operational, legal, and payer-specific depth that most blogs skip entirely.

What Is AOB in Medical Billing

AOB in medical billing stands for Assignment of Benefits. In legal terms, it is a written instrument by which the patient (the policyholder or insured) transfers their right to receive insurance benefit payments to the healthcare provider. Once executed, the insurer's obligation to pay shifts it must remit directly to the provider, not the patient.

|

Billing Precision Note: On a CMS-1500 claim form, the AOB authorization is captured through Box 12 (Patient's or Authorized Person's Signature) and Box 13 (Insured's or Authorized Person's Signature). Box 13 specifically authorizes direct payment to the provider. Many practices use 'Signature on File' (SOF) notations. This is legally acceptable only if you have a signed paper or digital AOB stored in the patient record. SOF without an underlying document is a compliance exposure. |

What Is the Purpose of the AOB

Most billers can answer what is the purpose of the AOB form at a surface level: it routes payment to the provider. But the form does several things simultaneously, and each function has legal weight:

1. Payment Assignment (The Core Function)

The patient formally delegates their right to receive insurance benefit payments. This creates a legal obligation on the insurer to pay the provider, not the patient.

2. Authorization for Information Release

The AOB authorizes the insurer to share claims data, EOB details, and coverage information with the provider's billing department. Without this, HIPAA creates friction in routine billing communication.

3. Provider Standing to Appeal

A signed AOB typically grants the provider the legal standing to file a first-level appeal, grievance, or even civil suit against an insurer for underpayment or wrongful denial. Without it, only the policyholder has standing — which means appealing a denial requires patient involvement in every step.

4. Defining the Scope of the Assignment

This is where most generic AOBs fail. The form must specify whether the assignment is for a single date of service, a specific procedure, or an ongoing blanket authorization covering all future services. An imprecise scope can be challenged by insurers, especially in payer audits or litigation.

A legally sound AOB form must include the following elements — not suggestions, requirements:

▸ Patient Identification: Full legal name, date of birth, member ID, and group number exactly as they appear on the insurance card.

▸ Provider Information: Legal practice name (not DBA), NPI (National Provider Identifier), tax ID, and billing address. One character difference from the payer's credentialing record is enough for a payment routing mismatch.

▸ Assignment Language: Clear, explicit language: 'I hereby assign all medical benefits and/or insurance reimbursements to which I am entitled to [Provider Name]...' Vague language like 'billing authorization' is insufficient.

▸ Scope Statement: Date(s) of service covered. If blanket, specify 'for all services rendered from this date forward' with a start date.

▸ Revocability Clause: Some forms include non-revocation language, particularly when the assignment is linked to a lien or EMS transport. For standard clinical practice, specify terms of revocation to avoid disputes.

▸ Patient Acknowledgment of Remaining Responsibility: The AOB assigns insurance benefits only. The patient must explicitly acknowledge they remain responsible for copays, deductibles, coinsurance, and any non-covered services.

▸ Signature and Date: Signed by the policyholder, legal guardian, or holder of power of attorney. Date is critical — it must predate the claim submission.

Who Signs AOB in Medical Billing And When It Gets Complicated

Standard Scenarios

▸ The Patient = The Policyholder: Most common situation. The patient is both the insured and the one receiving care. They signed, and the case was closed.

▸ Dependent Adult Children (Under 26): Patient may be covered under a parent's plan but is 18+. The patient signs, not the parent. The parent is the policyholder but the patient has legal authority over their own healthcare decisions.

▸ Minor Patients: A parent or legal guardian must sign. Verify guardianship if parents are divorced; the non-custodial parent may not have authority, and an improperly executed AOB can be challenged.

▸ Incapacitated Patients: Requires a Power of Attorney (POA) or court-appointed guardian. Collect and scan the POA documentation. Not all POA documents cover healthcare financial authorizations, verify the scope.

▸ Medicare Patients: For participating providers, Medicare's own participation agreement handles direct payment. However, the AOB still needs to be captured as the patient authorization. Non-participating Medicare providers who bill at limiting charge still need an AOB and must be aware that some Medicare Advantage plans have different assignment rules set by the plan, not CMS.

The Employer-Sponsored Self-Funded Plan Problem

This is the scenario that catches practices off guard. A patient with a Fortune 500 employer's self-funded health plan (administered by, say, Cigna or Aetna as a TPA) may have an anti-assignment clause embedded in the plan document — the SPD (Summary Plan Description). The patient has no idea. The front desk has no way to know from the insurance card.

The patient signs the AOB. The claim is submitted. The TPA adjudicates the claim and issues the check to the patient anyway, citing the anti-assignment clause in the underlying ERISA plan. The provider has no contractual relationship with the actual plan. The collection becomes a patient-level problem.

ABN and AOB in Medical Billing

|

Feature |

AOB — Assignment of Benefits |

ABN — Advance Beneficiary Notice |

|

What it does |

Transfers patient's right to receive insurance payment to the provider |

Notifies a Medicare beneficiary that a specific service may be denied as non-covered |

|

Who initiates it |

Provider collects from patient at intake |

Provider issues to patient before delivering a potentially non-covered service |

|

Who signs |

Patient or authorized representative |

Medicare beneficiary only |

|

Applies to |

All payers — commercial, Medicare, Medicaid, self-funded |

Medicare (traditional Part A and B) only |

|

Financial effect |

Routes insurance payment to provider |

Transfers financial liability to patient if Medicare denies |

|

When timing matters |

Must predate claim submission |

Must be issued before the service is delivered |

|

CMS-1500 link |

Box 13 — payment authorization to provider |

Box 20 / modifier GA, GX, GZ on line items |

|

Consequence of skipping |

Insurer pays patient instead of provider |

Provider cannot bill patient if Medicare denies — must write off the service |

The two documents can coexist. A Medicare patient receiving a potentially non-covered service needs an ABN (for liability protection) AND an AOB (for payment routing to the provider).

They are not substitutes for each other.

AOB and COB in Medical Billing & How They Interact in Dual-Coverage Claims

AOB and COB in medical billing are two separate but deeply intertwined processes. COB (Coordination of Benefits) determines which payer is primary and which is secondary.

AOB determines who receives each payer's payment. When a patient has dual coverage, both processes must be correctly executed or the billing can collapse.

How the Payment Flow Works with Dual Coverage + AOB

1. Eligibility verification confirms both plans, identifies primary vs. secondary payer per birthday rule, gender rule, or payer-specific coordination logic.

2. An AOB must be collected authorizing direct payment from both the primary and secondary payer to the provider. One signed form covering both is sufficient if the language is broad enough. Some practices use separate forms per payer for clarity.

3. Primary claim submitted. Primary payer adjudicates, issues EOB, pays provider directly (because AOB is on file).

4. Secondary claim submitted must include the primary payer's EOB showing what was paid. The secondary claim is the crossover claim.

5. Secondary payer adjudicates against the primary's payment, identifies the remaining balance, pays provider directly.

6. Patient owes only the confirmed final out-of-pocket amount remaining deductible, copay, or non-covered service balance.

Where COB + AOB Claims Break

▸ Missing AOB for the secondary payer is the single most common failure point. The primary payer routes payment correctly because you collected AOB at intake. The secondary payer has no AOB on file, so the secondary payment goes to the patient.

▸ Incorrect COB order. Submitting to the wrong primary payer results in the primary applying benefits that should have been secondary, creating a coordination headache that requires provider-initiated appeals with both payers.

▸ Medicare-Medicaid crossover claims. Medicare processes the claim and automatically crossovers the remainder to Medicaid in most states. Here, the AOB is embedded in the Medicare participation agreement, but the practice must verify that the Medicaid MCO (if applicable) will also honor direct payment.

▸ Auto insurance as primary. For accident-related injuries where auto insurance is primary, an AOB must be executed specifically for the auto liability or PIP (Personal Injury Protection) carrier, which operates under completely different rules than health insurance. Standard health insurance AOB language often does not cover auto payers.

AOB Best Practices

Most AOB failures are not legal failures; they are workflow failures. Here is how to eliminate the gaps that cost practices money:

At the Front Desk

-

AOB collection should be a mandatory intake checkpoint — not optional, not skipped for established patients. Policies change. Payers change. A patient who had commercial insurance last visit may have switched to a self-funded plan that has an anti-assignment clause.

-

Train front desk staff to explain the AOB in plain language, not legal jargon. Patients who understand what they are signing are less likely to dispute it later.

-

For patients unable or unwilling to sign, document the refusal, collect full estimated payment upfront, and flag the account in your PMS so billing knows not to rely on insurance routing.

In the Billing Workflow

-

Cross-reference your PMS/EHR to confirm a valid AOB exists before submitting every claim. Automate this check where your system supports it.

-

When a payer returns a claim with the payment going to the patient despite an AOB on file, do not simply write it off. Contact the payer's provider relations line, reference the AOB, and request reissuance. Most standard commercial payers will reprocess the payment if given documentation.

-

For Medicare patients, verify participation status per payer, per provider NPI. Group NPI and individual NPI assignment rules differ. A physician rendering under a group NPI must ensure the group's participation agreement covers the direct payment routing — individual NPI assignment alone does not always suffice at the group claim level.

For Document Retention

-

Store signed AOBs in a document management system attached to the specific patient account and encounter, not in a general folder. You must be able to pull the AOB on short notice during a payer audit or claims dispute.

-

Retain AOBs for a minimum of 7 years, or longer if your state mandates it or if the claim is subject to Medicare/Medicaid review. The statute of limitations for insurance fraud claims runs longer than most practices retain documents.

-

Digital AOB signatures are legally valid under the ESIGN Act and UETA, but your digital signature platform must produce an audit trail showing when, where, and by whom the form was signed. A simple PDF checkbox is not an enforceable electronic signature.

Final Words

AOB in medical billing is the difference between a practice that controls its reimbursement cycle and one that depends on patients to relay insurance checks.

When executed correctly with the right form language, the right CMS-1500 box population, awareness of anti-assignment clauses, and proper coordination with COB, it is the most powerful single document in your revenue cycle.

When executed lazily, blank SOF notations without underlying forms, generic AOB language that does not hold up under payer scrutiny, and no verification of plan-level anti-assignment provisions, it gives the illusion of control while leaving real money exposed.

Treat your AOB workflow as a compliance and revenue function, not a paperwork routine. Audit it quarterly. Train your front desk team on it. Have your forms reviewed by healthcare counsel annually.

The practices that do this collect faster, appeal more successfully, and spend significantly less time chasing patients for insurance money that should have come directly to them in the first place.

ABOUT AUTHOR

Tom Watkins

As a blog writer with years of experience in the healthcare industry, I have got what it takes to write well-researched content that adds value for the audience. I am a curious individual by nature, driven by passion and I translate that into my writings. I aspire to be among the leading content writers in the world.